How magnificent can the magnificent seven get?

How magnificent can the magnificent seven get?

Popping the hood on the S&P 500's performance...

The S&P 500 Index (SPX) represents the 500 largest corporations in the US by the value of their shares and is commonly used as a proxy for the US market since the index’s inception in 1957. By all accounts, the index has had a stellar 2023, currently sitting at c. 4,600, +19% YTD ex-dividends, near all-time highs.

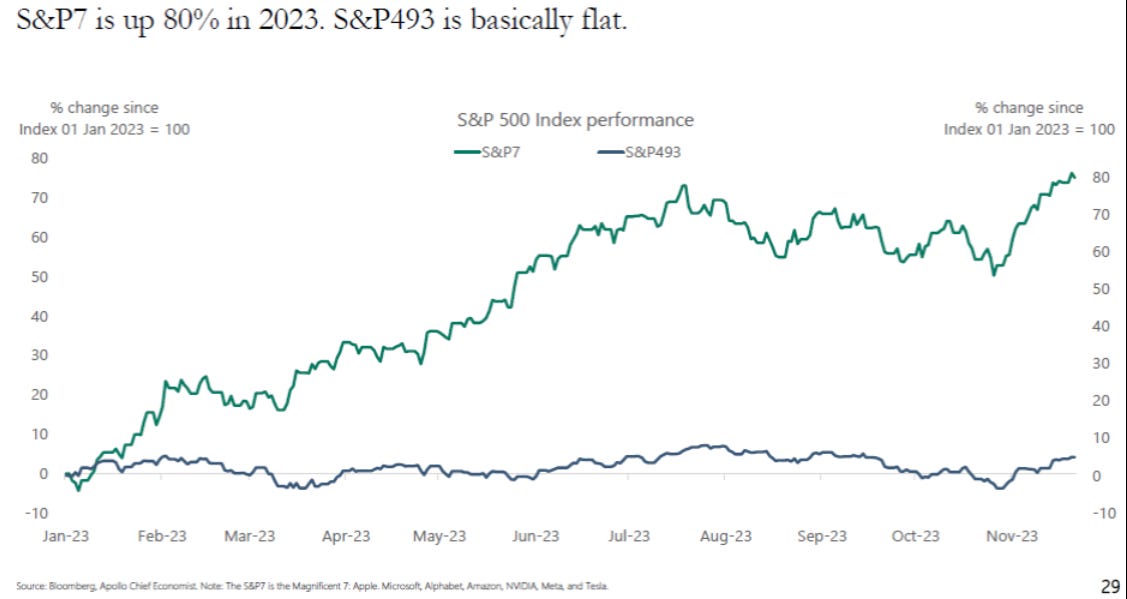

However, if one were to dig a little deeper and look at the drivers of this performance, a clear decoupling has happened between seven stocks within the index and the rest. These 7 stocks are known as the Magnificent 7 (M7) and include Apple, Amazon, Microsoft, Nvidia, Meta (Facebook), Alphabet (Google) and Tesla. On their own, these stocks represent 28.9% of the SPX index and are up, on average 80% YTD, compared with basically flat for the remaining 493 stocks of the index. This chart is truly astonishing…

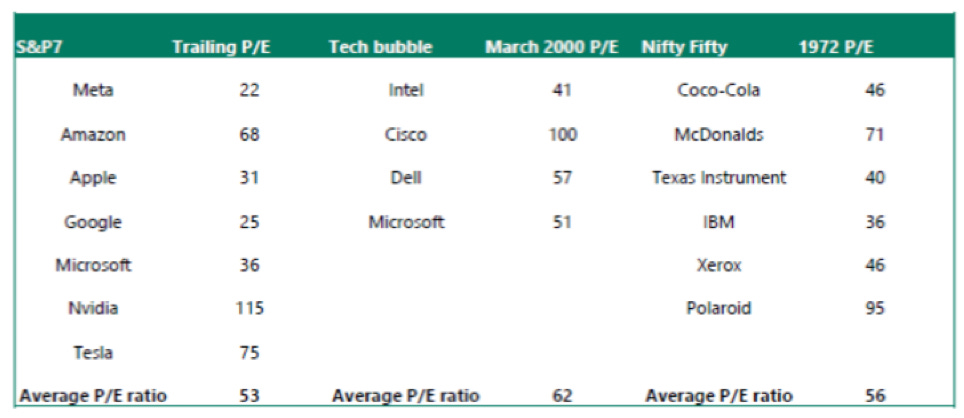

So we can conclude that this year’s market performance is in reality, the performance of big tech and not really a wider market trend. When looking at this trend, there are clear parallels between the M7 and a group of stocks that emerged in the 1970s known as the ‘nifty 50’, as well as tech stocks in 2000. In the case of the nifty 50 and tech in the 2000s, valuations eventually got very stretched. Below is an interesting chart put together by Apollo showing the current valuations of the Magnificent 7, which are approaching the levels seen with the Nifty 50 and tech stocks in 2000. Eventually, it all ended in tears, with the Nifty 50 crashing in the 70s and the dot.com bubble busting.

One of the biggest drivers of the decoupling in the SPX is mostly likely linked to the arrival of AI (Artificial Intelligence) in the mainstream, a general-purpose technology which the market believes is poised to have a transformational impact on productivity and economic growth across all sectors of the economy. Generally speaking (and this is a vast generalisation), the view is that big tech is likely to be the biggest beneficiary of this trend as AI is largely linked to data, and big tech controls the largest pools of data ever amassed in the history of humankind. We can conclude that the market right now is happy to pay high valuations in exchange for what could be high growth across the AI landscape for big tech companies.

The broader point here is that while the M7 are unquestionably great companies, and many of them are mature tech that produces strong cash flow (namely Apple, Microsoft and Amazon), great companies can also turn into poor investments at given periods of time when valuations get too stretched.

The intention of this post is not to go into a deep debate about whether these stocks are mispriced or not but to make investors aware that when buying the SPX, they are putting their money into an index that is not as diversified as has been the case historically with a large concentration on the M7, at a time where valuations of these stocks are ‘high’ for historical standards.

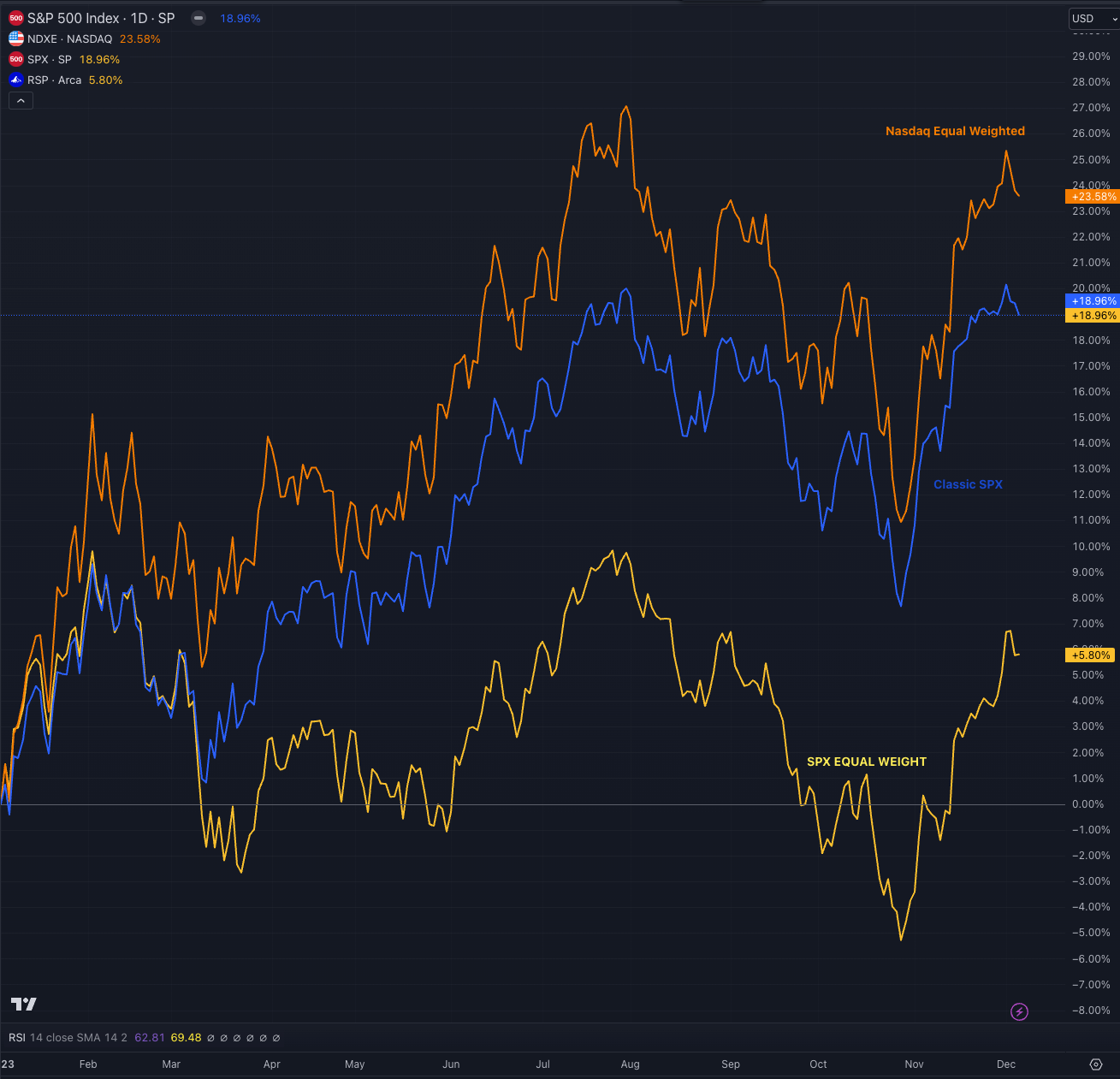

So, are we saying stay away from big tech? Not at all. Given their importance and the potential new paradigm shift with AI, it would probably not be a prudent strategy. What can we do as investors if we want exposure to the M7 but not in an ill-diversified way like a market cap-weighted index SPX? Instead of going long the SPX index, we would look to towards an equally weighted Index (ticker EWI). If you are more interested in gaining exposure specifically to tech, an equally weighted Nasdaq-100 Index (ticker NDXE), would probably be the way to go. Interestingly, when you put the SPX, EWI AND NDXE against each other on a chart, NDXE comes out on top! Food for thought…

Nothing is perfect, and by going long the NDXE, you will be investing in a lot of unprofitable tech companies that are decently levered and have been battered as rates have climbed higher. Some of these companies might struggle to refinance their debt at higher punitive rates over the next few months…

This is all for this week. As always, this is not investment advice, do your own research.

Until next week!

Niki and Tom